This comprehensive guide has been developed to help you, the busy agency nurse, to better understand everything that may be puzzling you around pay rates and payment options. We aim to simplify the confusion around framework pay rates, umbrella companies, limited companies and much more to ensure you can make informed pay rate and payment choices that best fit your unique situation.

Each section of this guide looks to answer the questions that we know agency nurses ask, in a way that is easy and quick to understand (because we know you have better things to do), and simple to share.

If you still have unanswered questions, please feel free to contact us and we will do our best to help.

Pay Rates

What's the pay rate?

Probably THE MOST frequently asked question in the world of agency nursing. And for good reason. After all, if the UK’s most trusted profession doesn’t deserve to be remunerated well for their work efforts, who does? Yet, while the answer is often quite simple, there are so many factors at play that often times, it can seem quite the opposite. So, what's causing this confusion?

Well, the initial structure of an hourly pay rate is simple enough as it's based on a nurse's band (grade) and what time of the day, or week the shift will occur. However, when you start factoring in other variables such as client type, agency type, pay caps and payment type, things start to get a bit more complex.

NHS agency pay rates in the UK

Pay rates for nurses working agency shifts within the NHS are subject to whether their agency is on an NHS framework, or 'off-framework' and also vary according to pay caps and rate escalations, but policies differ in each UK country. Rates are also different when you're paid via the PAYE system, as opposed to via an umbrella or limited company. Even things like whether your agency operates 'rolled-up holiday pay' and includes travel expenses will affect that all-important hourly pay rate.

NHS agency pay rates in England

NHS pay rates for temporary staffing in England are managed by three separate framework providers. Nursing agencies sign up to these frameworks in order to be able to supply the NHS with agency staff. Each framework operates its own set of rates (framework rate cards) for various types of nurse bands, specialties and shifts. While framework rate cards abide by NHS Improvement rate caps, frequent rate escalations and other factors mean that framework agencies are often juggling multiple rate cards for England at any given time.

So, while we are unable to publish an England rate card (like we have for Scotland and Wales below) the answer to the number one question "What's the pay rate?" is only a short phone call or email away.

To learn what the pay rate is for any Medacs Healthcare nursing job in England - NHS and private - contact our England & Wales Team on 01785 236 202 (during office hours) or via the contact form below.

Click here to view NHS Framework rates in Scotland.

For further information on all Medacs Healthcare's Scotland nursing pay rates - NHS and private - simply contact our Scotland Team on 0141 225 5451 (during office hours) or via the contact form below.

NHS health boards in Wales only have one framework provider to comply with that operates their own rate caps.

Click here to view NHS framework rates in Wales.

For further information on all Medacs Healthcare's Wales nursing pay rates - NHS and private - contact our England & Wales Team on 0800 442 207 (during office hours) or via the contact form below.

In Northern Ireland the NHS is commonly known as the HSC (Health and Social Care). Like the NHS, the HSC works with framework providers for temporary staffing and complies with pay caps that are specific to this country.

Medacs Healthcare is not on any framework in Northern Ireland and is therefore, unable to offer agency work to nurses in Northern Ireland at this time.

Agency nursing pay rates explained

As we can see, pay rates for agency nurses in the UK vary depending on multiple factors. Here's a comprehensive list that explains these factors in more detail:

Instead of earning a ‘salary’ like a substantive nurse does, an agency nurse is paid an hourly rate that varies depending on their setting, specialty and shift type. Typically, nurses working within general medical or surgical settings are paid one rate while nurses working in specialty areas like A&E, ITU, community and certain mental health settings, are paid at a higher rate for work in the NHS.

Outside of this, only the ‘practitioner’ roles, such as Emergency Nurse Practitioner (ENP) and Advanced Nurse Practitioner (ANP), are paid at a further enhanced rate due to the seniority of the position. These rates are further broken down by shift type, typically; weekdays, week nights, weekends and bank holidays, with the latter and sometimes Sundays commanding the highest pay rates available.

The main types of clients that recruit nurses in the UK are the NHS and private sector organisations such as private hospitals and nursing homes, to name but a few.

Some Her Majesty’s Prisons (HMPs) are managed by the NHS and some are privately run; both types recruit agency nurses. Pay rates vary between client types and individual clients (more so in the private sector), so while there will always be speculation about which pays more - NHS or private - there is no definitive answer.

Not all nursing agencies play on a level playing field when it comes to pay rates. This is because there are NHS framework agencies and non-framework agencies. In temporary healthcare staffing, a framework is a list of approved suppliers who have been vetted and audited by a framework body to provide assurances to clients that they can supply staff of high quality and at a competitive price.

There is one framework that covers Scotland, a different one for Wales and three others for England; each with their own set of rates. So an A&E nurse who works a weekday shift at an NHS hospital in Scotland for instance, will earn a different rate to the same specialty nurse in Wales or England.

Non-framework agencies, as the name suggests, are not bound by framework agreements or capped rates. However, this usually comes with the trade-offs of short-notice shifts at long distances, that are few and far between.

Pay rate caps were introduced in 2015 by NHS Improvement in an attempt to decrease the amount of money the NHS spent on agency staff. While the intention was to direct nurses away from agency work back to substantive posts, what actually happened initially, according to Medacs Healthcare's Operations Director of Specialist Staffing was nurses were leaving NHS hospital wards to such an extent that it drove trusts to regularly breach pay caps by issuing rate escalations.

This still happens today. So, when a trust has concerns over patient safety - caused by factors such as severe shortages of permanent or bank staff, a sudden rise in demand for more specialist nurses or winter pressures - it exercises its right to use the ‘break glass’ provision under NHS Improvements’ ‘Agency Rules’ regulations. What this means is that any NHS organisation can issue nursing agencies with escalated pay rates that temporarily override rate caps or framework agreements for either a specific setting, specialty or shift type.

While pay caps remain the core foundation of framework agreements across England, Wales and Northern Ireland (rate caps have never applied in Scotland), they are not a one-size-fits-all solution.

Common reasons for pay escalations

- Remote locations - the more remote a hospital, the more challenging it is to fill rotas with enough staff to ensure patient safety. Nurses who work in remote locations are still likely to get paid higher rates to compensate for travelling further

- High off-framework spend - in areas where agency staff were paid high rates before the rate caps came in, it was always going to be difficult to switch these nurses to (in some cases much) lower capped rates

- Seasonality - from October, many trusts escalate their rates to provision for ‘winter pressures’ which is where many hospitals see an increase in patient numbers during the colder winter months

- Specialty shortage - as is often the case with A&E nurses in some areas, some specialties are issued with rate escalations purely down to increased demand

If you are paid via your own limited company (also known as PSC, or personal service company) you will often be quoted a higher pay rate than if you are paid via a PAYE system. This is to compensate for any employer costs (such as Employers National Insurance) you or your umbrella company need to pay when you file your annual self-assessment tax return.

Any work assignment that you do as a limited company nurse - which the trust has deemed to be ‘inside IR35’ - has tax and National Insurance deducted ‘at source’ by the trust, which effectively means that you are paid the PAYE rate.

Some nursing agencies artificially inflate their pay rates by adding holiday pay. This practice, commonly known as ‘rolled-up holiday pay’, is actually against a ruling made by the European Court of Justice. The Government's guidance on holiday pay confirms that holiday pay should only be paid for the time when annual leave is taken.

Medacs Healthcare does not practice ‘rolled-up holiday pay'. The pay rates we offer are always the true hourly rate. However, we realise that you might still want to understand what the pay rate is including holiday pay in order to easily compare rates. So for this reason, we are happy to provide you with the calculation in our rate cards and over the phone. Instead of rolling-up the holiday pay into our pay rates, we encourage our nurses to claim their full allowance of holiday pay as and when they need it.

Typically, travel expenses are not included in agency nursing pay rates within the NHS. However, community nursing is the exception, as travel expenses are paid separately. Some agencies offer incentives to attract certain types of nurses to certain areas. At Medacs Healthcare, we pay mileage for our community nursing roles.

Pay rates also fluctuate when there are changes to worker regulations, framework contracts and government updates such as pensions and minimum wages.

Tax and National Insurance

As much as we might like to, there is simply no avoiding tax and National Insurance in the UK. Both play a huge part in everyday life and are vital to society.

While the majority of money that an agency nurse earns is transferred directly from the employer to the nurse, there are certain deductions that must be made. But what is tax and why is it levied directly on personal income? Likewise, National Insurance - is it possible to reduce the amounts that are deducted?

Tax is a percentage of your personal earnings which is retained by the government and used to fund public services such as healthcare, education, transport and welfare. Commonly referred to as income tax, this money can come from a number of sources, depending on your circumstances. These include:

- Income from employment

- Income from pension

- Income from a trust

- Interest on savings

- Employment benefits

- Rental income

Income tax can be paid in one of two ways. Pay as you earn (PAYE) income tax is deducted from your salary by your employer (nursing agency, umbrella company or your limited company), while self-employed taxpayers file a self-assessment tax return on an annual basis and pay any outstanding income tax as part of that process. Individuals with complex sources of income or legacy complex tax positions may also be requested by HMRC to complete a self-assessment tax return.

Tax Rates and Bands

The amount of income tax you pay each year depends on your overall earnings. There are different rates which determine what percentage of your income is retained by the government. These are based on a standard Personal Allowance of £12,500.

The current Income Rates and bands for England, Northern Ireland and Wales are available here.

These rates differ if you live in Scotland, move to or from Scotland, own a home in Scotland and one elsewhere in the UK or stay in Scotland on a regular basis.

If you earn over £12,500 over the course of a financial year (6 April to 5 April), then paying tax is unavoidable. In fact, avoiding paying tax (also known as tax evasion) is actually illegal and carries very strict penalties that range from a hefty fine of up to 200 per cent of the total tax owed to time in prison.

Some agency workers have been known to work through non-reputable umbrella companies that make 'too good to be true' claims such as being able to offer you greater take-home pay. In all likelihood, these are the types of umbrella companies that operate tax avoidance schemes. HMRC has made a number of legislative changes over the past few years in order to pursue individuals and organisations such as umbrella companies for non-payment of tax under certain schemes.

Failing to pay the correct amount of tax is illegal, so agency nurses are advised to select their umbrella company with caution.

Tax Allowances and Relief

While there is no way to avoid paying tax, there are certain allowances and reliefs that can reduce the amount of tax you pay. The first £12,500 of income earned in a financial year is tax-free and broken down into weekly/monthly allowances; this is known as a Personal Allowance and applies to those with an annual income of less than £125,000.

Your Personal Allowance can be smaller if you are married and earn less money than your spouse, as a ‘Marriage Allowance’ allows you to transfer up to £1,250 of your Personal Allowance to your husband, wife or civil partner. This can reduce their tax bill by up to £250 over the course of the tax year.

Agency workers who are paid through their own limited company, may also be able to apply certain tax reliefs that, when combined with careful tax planning, can generate higher levels of take-home pay compared with PAYE or umbrella company nurses.

You may also be able to claim tax relief on work-related expenses including uniform, travel and overnight accommodation if these are not provided by your employer.

If you are unsure about how much tax you should be paying it might be worth using one of the many tax calculators available online that help you calculate whether you are paying the correct amount of income tax. Unfortunately, estimates are only available for pay as you earn (PAYE) taxpayers.

Form P45 is issued when you stop working for an employer. The P45 shows the amount of tax you have paid so far in the tax year (6 April to 5 April). A P45 has four parts (Part 1, Part 1A, Part 2 and Part 3).

Your employer sends details for Part 1 to HMRC and gives the other three parts to you. You should keep Part 1A for your own records and give Parts 2 and 3 to your new employer (or to Jobcentre Plus if you're not working). You can't get a replacement P45, so keep your P45 in a safe place.

Form P60 is a summary of the amount of tax paid on your income in the tax year (6 April to 5 April). You will need your P60, which are only available for current employees at the end of each tax year, to prove how much tax you have paid.

For example, if you wish to claim back overpaid tax, submit a tax return, apply for tax credits or use as proof of income if you apply for a loan or mortgage. It is advisable to also keep your P60 in a safe place.

National Insurance (also known as NI or NIC) contributions are paid by employees and employers and entitle workers to certain state-funded benefits such as the State Pension, maternity pay and unemployment benefits. National Insurance contributions apply to all workers over the age of 16 earning more than £166 per week.

There are different types of National Insurance (known as classes) and the type you pay depends on your employment status, how much you earn and whether you have any gaps in your National Insurance record.

Before you can start making contributions, you will require a National Insurance number. This unique nine-digit alphanumeric code ensures all your National Insurance and tax contributions are recorded against your name.

Your National Insurance number can also be found:

- On your payslip

- On your P60

- In your personal tax account

- On letters regarding tax, pension and/or benefits

Umbrella Companies

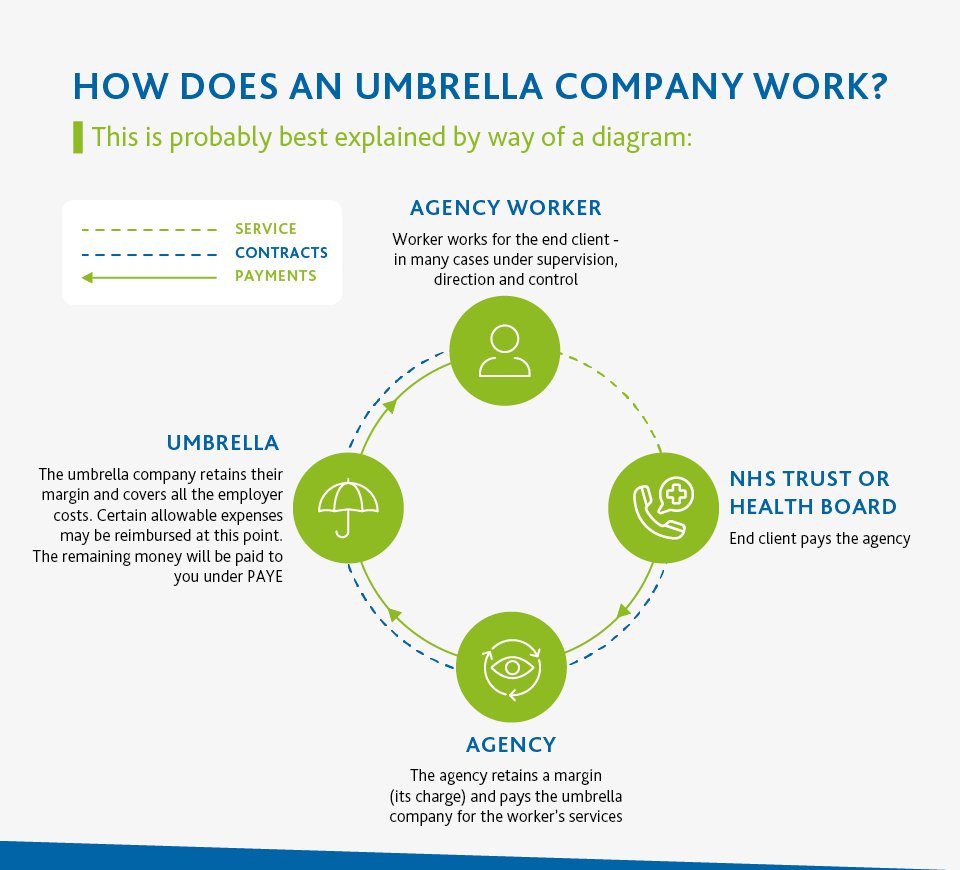

What is an umbrella company?

An umbrella company is a business that acts as an employer on behalf of an agency worker (often called a ‘contractor’). In its role as an employer, the umbrella company is ultimately responsible for paying workers, allowing for any necessary deductions (e.g. tax, National Insurance, student loan repayments, etc.), as well as processing timesheets and invoices.

The rise of agency nurses using umbrellas has come about, partly due to some agencies no longer wanting to deal with pay themselves and partly because of some umbrella companies offering models that do not apply standard PAYE-style income tax and National Insurance deductions and therefore increase the workers’ take-home pay. Such models are more risky to the agency worker and are subject to increasing scrutiny and challenge from HMRC.

The notion of working through an umbrella company might sound complicated, but the process is really quite simple. So, how do umbrella companies work?

Nurses who work through umbrella companies should see little or no difference in their take-home pay, to those who are paid through other methods. If the umbrella is a reputable one and deducts tax and National Insurance (NI) in accordance to HMRC rules, then a nurse’s take-home pay will roughly be the same as what they would have received via an agency’s PAYE system. However, some umbrellas will charge a fee for their services which will be deducted from take-home pay. We feel it’s important to reiterate that some umbrellas offer payment models that don’t deduct the correct levels of tax and National Insurance; a practice that is highly risky for an agency nurse.

Some umbrella companies offer ‘perks’ to try to attract agency workers but these may not actually be worth much or offer little value, so it’s always worth spending time weighing these things up when it comes to deciding on your umbrella company.

To operate under an umbrella company, you will have to pay fees on either a weekly or monthly basis. These fees tend to range from £15 to £30 per week, while the difference in monthly charges varies slightly more at between £80 and £130. These fees can vary depending on the umbrella company you choose.

Nurses who work through umbrella companies should see little or no difference in their take-home pay, to those who are paid through other methods. If the umbrella is a reputable one and deducts tax and National Insurance (NI) in accordance to HMRC rules, then a nurse’s take-home pay will roughly be the same as what they would have received via an agency’s PAYE system. However, some umbrellas will charge a fee for their services which will be deducted from take-home pay. We feel it’s important to reiterate that some umbrellas offer payment models that don’t deduct the correct levels of tax and National Insurance; a practice that is highly risky for an agency nurse.

Some umbrella companies offer ‘perks’ to try to attract agency workers but these may not actually be worth much or offer little value, so it’s always worth spending time weighing these things up when it comes to deciding on your umbrella company.

What are the pros and cons of umbrella companies?

When it comes to deciding how to receive payment for the work you complete, the umbrella company route is quite a popular option. It's not just agency nurses...other contractors such as locum doctors are also opting in, or in some cases, are obliged to jump aboard the umbrella company bandwagon. So what are the advantages for healthcare professionals pursuing this method of employment and are there any downsides?

As with so many of life’s decisions, there are positive and negative issues which must be considered. It’s up to you to decide whether the positives of joining an umbrella company outweigh the negatives. So, which route is best for you?

The Advantages

Joining an umbrella company is traditionally viewed as being a simple method of contracting. Most providers offer hassle-free registration and can usually have you up and running in a few hours. Ideal if you are eager to enter into the exciting world of agency nursing.

One of the major advantages of using an umbrella company is that the administrative responsibilities on your part are minimal. Umbrella companies will take care of all of your invoicing and payment chasing, as well as the majority of miscellaneous paperwork that happens to come your way. In general, actions are carried out by the umbrella company or Her Majesty’s Revenue and Customs (HMRC).

In addition to handling the majority of your paperwork, some umbrella companies will also process your payroll under the PAYE scheme. This means that the provider will deduct income tax and National Insurance contributions, as well as any other fees that may be owed, such as student loan repayments, from your salary. Such a service would not be available to those working through their own limited company.

As you are under contract, you are legally an employee of the umbrella company. This means that you are entitled to certain benefits including sickness pay, maternity/paternity pay and holiday pay.

Finding the right umbrella company to meet your needs is important. Understandably, you may have plenty of questions about operating as a contractor and umbrella companies are likely to be able to provide answers. This can be an incredibly useful resource, particularly on issues like changes to legislation.

Although there are plenty of positives to working as an agency nurse, it’s a career path that doesn’t suit everyone. Working through an umbrella company allows you the opportunity to work independently without having to start your own limited company. This low-risk approach means that you can easily return to full-time work at any time. It can also help to reduce your admin should you work for multiple agencies.

Disadvantages

While using an umbrella company does have its benefits, there are certain drawbacks.

Arguably, the biggest challenge is knowing which umbrella companies you can trust. Finding a reputable provider is vital and could save you money in the future. Use extreme caution with any umbrella company that promotes 95, 90 or even 85 per cent take-home pay. Unfortunately, their methods are not approved by HMRC and the risks of using a non-reputable umbrella company could leave you with a very large tax bill.

One of the major positives of operating as a contractor is a sense of freedom. Unfortunately, working through an umbrella company does restrict your financial control more than it would if you were to operate through your own personal service provider.

While working through an umbrella company may mean less paperwork, you are still required to complete timesheets and expense claims, tasks that can prove tricky, especially if you’re unfamiliar with either process.

Payment through an umbrella will mean that you miss out on certain tax benefits associated with having a limited company. This is because the umbrella company deducts income tax and National Insurance contributions from your salary before it reaches your account.

While this method of payroll does save time and negates the need for you to submit payments to HMRC directly (an advantage for many contractors), it does mean that you lose out on some tax benefits afforded to independent company owners.

Umbrella companies also charge for their services. This fee is deducted from your earnings, along with income tax and National Insurance. These costs vary between providers, although a rate of around £30 per week is considered to be the average. However, it is worth enquiring about monthly charges, which can be slightly lower at about £80.

PAYE, Umbrella or Limited Company?

So, we’ve talked about umbrella companies, how they work and answered some of the burning questions we know nurses have about them. But how do they compare with the other two payment options? And, more importantly, which option should you choose?

Before we get into helping you make an informed decision about which payment option might suit you best, let’s first touch on what PAYE and limited company options are.

What is PAYE?

PAYE, which stands for ‘pay as you earn’, is a method through which most employees in the UK pay income tax.

Before any money is transferred to your account, your employer will deduct income tax, which is calculated based on your tax code. The main element that affects the amount of tax you pay is your annual earnings, but there are also certain allowances and deductions that can also be taken into account. This money is then paid over to HMRC. Depending on your circumstances, National Insurance contributions and student loan repayments may also be deducted from your pay using PAYE.

Some agencies have moved away from PAYE in order to reduce their administration costs. Instead, they now invite their workers to use umbrella companies, through which PAYE is available.

What is a limited company?

A limited company can sometimes be a more tax-efficient method through which some agency nurses work and receive payment. Sometimes referred to as a PSC (personal service company), a limited company allows the holder to split their income between salary and dividends, which means there may be opportunities to render parts of their overall income unaffected by certain taxes including Class 1 National Insurance Contributions.

By establishing a limited company, you are able to operate as the director of your own company. This allows your limited company to potentially receive higher rates of pay from those clients and agencies who will work via this method and take advantage of certain other tax planning methods and reliefs.

Depending on assessments (such as IR35 assessments) carried out in relation to your contracting arrangements, tax and National Insurance may automatically be deducted from your payslip before payment is made to your limited company, which will need to be taken into account when you complete your annual tax returns. Deductions of tax at the time of payment to your limited company may well mean that you will not need to make as large a one-off payment once your annual self-assessment is complete and your final tax bill calculated.

You may, however, find that your taxation calculations become more complicated and you may, therefore, wish to engage the services of a taxation professional to assist you with this.

It is also worth noting that not all NHS organisations accept agency staff who wish to be paid via a limited company.

Due to the often ad hoc nature of agency work, some clients and agencies do not wish to shoulder the administrative burden that comes with a standard employment relationship. Therefore, some clients and nursing agencies may have a preference for workers who work through a limited company. The limited company acts as an additional buffer between the employer and the employee, preventing the need for an employment relationship and allowing the contractor to work on an ‘as needed’ basis.

Agency nurses who set up and work through their own limited company may be able to generate higher levels of take-home pay through the application of certain tax reliefs and careful tax planning.

As a director of a limited company you must:

- Follow your company’s rules

- Calculate your own tax and National Insurance deductions, as well as pay this money over to HMRC

- Keep company records

- File your accounts and your company tax return

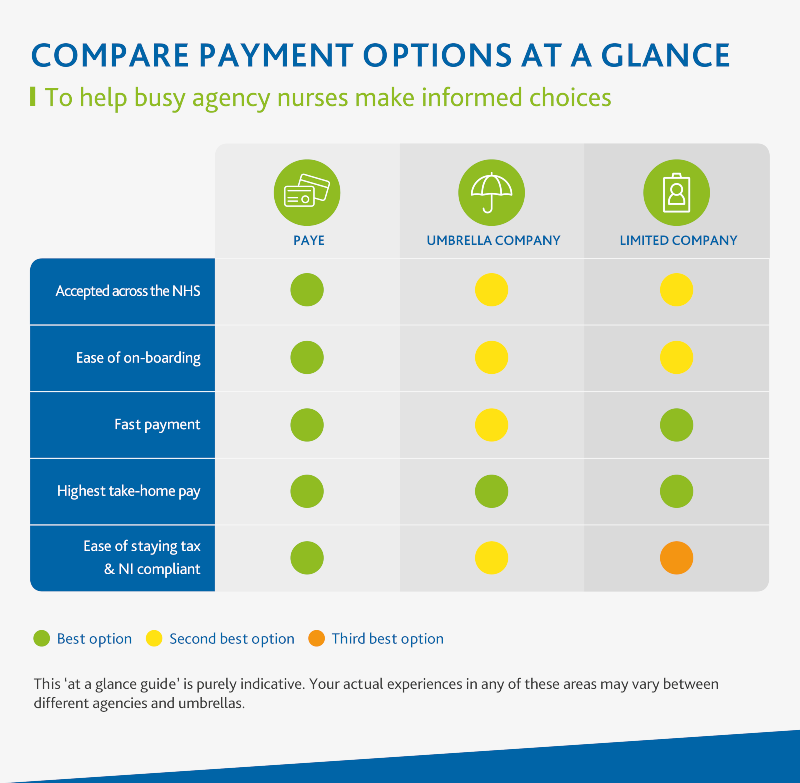

Which payment option is best for me?

Choosing whether to stick with your current payment option or change it in favour of a different one is a decision that deserves thorough consideration. Not only will it depend on your individual circumstances and whether your choice of agency deals with the payment option in question, but it also depends on which benefits are most important to you.

Hopefully, this handy comparison chart will set you in the right direction.

Additional guidance is supplied below:

- Different NHS organisations such as trusts and health boards have slightly different rules around acceptable methods of payment.

- Medacs Healthcare and other agencies offer PAYE and generally accept both umbrella company and limited company as payment methods, subject to any restrictions from the trust or health board.

- You may find that some agencies are selective about which umbrella companies they work with, Medacs Healthcare being one of them.

- On-boarding (also known as registration) procedures for the varying pay methods will differ from agency to agency.

- In general, you will find that on-boarding for PAYE workers constitutes a single form requesting personal, taxation and banking details.

- For umbrella companies you will generally need to provide your personal, taxation and banking details to the umbrella.

- To on-board with an agency for payment via an umbrella, you may find that the umbrella company will need to sign a supplier contract and provide a copy of your employment contract with them, which could add some time to the on-boarding process.

- If you want to work through a limited company, the agency is likely to ask you for more documentation to complete your on-boarding and may include - but isn’t limited to - providing a copy of the Certificate of Incorporation, VAT certificate (if applicable) and company bank details.

- The agency may also ask your limited company to sign a supplier contract and ask if you would like to be set up with self-billing.

- Some agencies will run a payroll daily, others weekly, so you should familiarise yourself with the payroll frequency of your chosen agency.

- Providing there are no issues with your timesheet or other requested information then, as a PAYE worker, your pay will be sent out following the completion of a payroll. This may then take between one and three days to arrive in your account, depending on the payment type chosen by your agency.

- Where you are being paid via your limited company, you will need to provide an invoice (or agree to self-billing) along with your timesheet so that your agency can pay your limited company to the terms agreed in the contract.

- Under the right circumstances, payment via a limited company can be just as quick as being paid via PAYE. However, different agencies will have different numbers of supplier payment runs in a week, so it's best to check with your agency on how they will do this.

- Payment via an umbrella company adds another party to the chain, which may result in your pay taking longer to get to you. When you submit your timesheet to the agency, your umbrella will submit an invoice to match or agree to self-billing). The agency will send the funds to the umbrella and they will then need to payroll this before they send you your pay. The time this takes will vary from umbrella to umbrella so you should look to understand how often your agency will do payment runs to your umbrella and then how often your umbrella will run a payroll.

- Since 2017, changes in IR35 legislation and action from Her Majesty’s Revenue & Customs (HMRC) have been enacted with one underlying principle in mind; that (broadly speaking) agency workers should be contributing proportionally the same income tax and National Insurance as permanent workers doing a similar job

- As such whether you are paid PAYE, via an umbrella or via a limited company, there shouldn’t be significant differences in your take-home pay

- If you are working a role that is classified as 'inside IR35' and you are a PAYE or limited company worker, you will see that the agency making the payment will deduct income tax and National Insurance contributions

- If you use an umbrella company, you will see that the umbrella will make these deductions

- If you have a limited company, you may be able to structure how your company pays you to take advantage of different or lower taxation rates (such as those on dividends) to legally improve your take-home pay. However, this kind of tax planning is often complex and we recommend you take advice from a taxation professional, specific to your personal circumstances. You may also find that you need to pay more tax via self-assessment

- Be wary of umbrellas who quote very high rates of take-home pay

- When you are paid PAYE by your agency, you should be able to take significant comfort from that fact that your employer will ensure that the correct deductions are made as it's their job (not yours) to keep up to date with the relevant changes in legislation that affect your tax and pay

- Should you sign up with a reputable umbrella company then, they too, will ensure that correct deductions apply

- Those umbrellas who quote low rates of tax and high rates of take-home pay are more likely to put you at significantly higher levels of personal risk with HMRC, as they may not be ensuring your compliance

- Using your own limited company is much more complex from a tax and NI compliance perspective and the responsibility for this, sits with you as a director of that company.

- For peace of mind we recommend that agency workers with limited companies employ the services of a professional accountant or tax advisor

Understanding your Payslip

While they’re not exactly the most riveting of reads, reviewing and understanding your payslip – especially if you work through an umbrella company – is an important task but one we know you might need a little help with. Having an understanding of the most common deductions means you’re more likely to understand your payslip and more importantly if you’re being paid correctly - or not.

We start by uncovering some of the mysteries around umbrella company payslips and then take a deeper dive into other deductions such as student loans and pensions. We also cover off expenses and how to claim them as an agency nurse.

Umbrella payslips

All umbrella’s do things differently so there is no guaranteed way your payslip will look. So we’ll try and take you through some of the items you may not be expecting to see.

If you are a PAYE worker, when you talk with your agency it is most likely that rate you agree will be a basic pay rate. That is the rate on which you’ll pay personal tax and National Insurance.

However, your work will also attract Employers National Insurance and may also be eligible for holiday pay under Working Time Regulations. When your agency charges the NHS trust that you ultimately work for, it will include these costs in the rate charged. It will also include these costs in the amount it pays to your umbrella company. The umbrella will then pay over the Employers National Insurance elements to HMRC and will hold eligible holiday pay for you until you claim it.

One of the common things that umbrellas may do on your payslip is show you how they have broken down all the funds they have received from your agency and so they may start with a total value and show Employers National Insurance and holiday pay as deductions. Once they have done this the amount remaining should be the same as the basic pay rate you have been quoted multiplied by the hours you have worked. From there you will see PAYE and NI deducted to then arrive at the net pay they will pay into your bank account.

This total rate (including Employers National Insurance and holiday pay) paid to your umbrella is often referred to as the 'Limited Company Rate' and is also a rate you may be quoted should you request to work through your own limited company. This is because your limited company is your employer and will need to pay over Employers National Insurance to HMRC on your behalf.

Student loans

If you are a fully qualified nurse, there is a good chance that you studied nursing at university, a route that can bring with it a considerable amount of debt. Understandably, there are plenty of questions that need to be asked, like when does this debt need to be repaid and will it have a significant impact on your future finances?

Prior to 2017, student loans for nursing degrees were provided by the NHS in the form of bursaries. These funds were intended to cover the fees charged by universities and meant that nursing students only needed to take out a student loan to cover maintenance.

However, following NHS bursary restrictions, many trainee and newly-qualified nurses, midwives and allied health professionals must now take out student loans in order to fund their education too.

The average student loan debt for a nurse varies, depending on where and when you attended university. For example, a nursing student who qualified in the 1990s will typically be lumbered with less debt than a student nurse who qualified more recently.

Today, the average student loan debt for a newly qualified nurse is over £50,000. This is a staggering amount of debt, especially when you consider that the starting wage for a fully qualified nurse is between £22,000 and £26,000. So how do you pay off this debt?

For nurses, the method by which a student loan debt is repaid is no different from that of any other university student. Repayments typically begin in the April after you have graduated and continue throughout your working life, providing you meet the minimum threshold for repayment.

The amount you will repay depends on what repayment plan you’re on and then only if your income is above the repayment plan threshold.

Student loan repayments for nurses through a personal service company are slightly different. As you are technically an employee of your own company, it is your responsibility to declare your student loan when completing a self-assessment personal tax return.

If you still have a sizeable university debt and you are afraid that you will never be able to repay it, don’t worry. Depending on your plan type (1 or 2), student loan debt has an expiry date which means you won’t necessarily have to repay the full amount.

Pensions

Ensuring you have adequate savings for later life might seem like a scary prospect, but making regular contributions towards your pension pot during your working life can help prevent the need for fear. The UK government even lends a helping hand, providing tax relief on payments made towards your pension and providing a State Pension.

A pension is a way of saving regular amounts of money throughout your life. All workers are encouraged to make regular contributions so that they do not have to rely on the state when they reach the State Pension age. If you are a member of a workplace pension scheme, contributions towards your pension are deducted from your pay, along with both tax and National Insurance. This means that, once these deductions have been made, the figure in your final payslip will be slightly lower.

Throughout your working life, you may acquire a number of pension funds, depending on how many different agencies or direct employers you work through. Should you switch schemes, don’t worry; any money amassed under a previous pension scheme will remain yours and will be made available once you retire. Alternatively, you can continue paying into a previous pension scheme, transfer your pension to your current scheme or begin drawing your pension (providing you are eligible to do so).

As a PAYE agency nurse, you are entitled to some of the same rights as any other employed person. These rights include a pension (providing you meet the minimum earnings threshold), the minimum wage and holiday pay.

Employers now offer ‘auto-enrolment’ pension schemes. This means that an employer must enrol all of its 'Eligible' job holders into a qualifying workplace pension scheme if they are not already in one. Any worker who is not automatically enrolled will have a right to opt in or join the scheme.

An Eligible job holder is one who meets the following criteria:

- Earn at least £10,000 a year

- Aged over 22 or under State Pension age

- Working in the UK

Pension schemes generally include contributions from employers as well as employees, though these vary from scheme to scheme. The employer contributions are generally subject to a certain/minimum level of employee contributions. Some employers may choose to pay more than the statutory minimum, you should check the details from your employer or the pension scheme provider if you would like to know more.

You cannot opt out of the automatic enrolment process, as your employer is obliged to enrol you into a pension scheme. However, you can opt out of membership of the scheme once you have been enrolled.

If you opt out within one month of the start of the opt-out period, you should be treated as if you had not been a member of the scheme and a refund of any contributions deducted from qualifying earnings should be given. This can be done by completing the opt-out notice form and sending it to your employer or pension provider.

However, if you opt-out outside of this period, your pension scheme membership will be stopped. You may be able to receive a refund of contributions but this will depend on the pension scheme rules.

If you are a PAYE worker of Medacs Healthcare, you are not an employee of an NHS Trust and are not, therefore, eligible to join the NHS pension scheme. You may be enrolled in our Automatic Enrolment pension scheme, providing you meet the eligibility criteria.

If you are being paid directly by the Trust via a direct engagement model, your classification as an independent contractor means that you are not an NHS employee and therefore you are not entitled to join the NHS Pension Scheme.

If you are being paid into your personal limited company, you are classed as an employee of that personal limited company and therefore you are not entitled to join the NHS Pension Scheme.

The State Pension is available to all workers when they reach the State Pension age. Once you have reached this age, you can start to draw the State Pension. The age from which you can normally start to draw your personal pension is 55, however, this may increase in line with the State Pension age.

In the event of ill health, you may be permitted to access your pension pot before the age of 55, though you must meet certain criteria set by the UK government.

How do I claim expenses?

Life as an agency nurse grants you the freedom to work whenever and wherever you want. But this career choice can often see expenses add up, especially when travel is considered. So what expenses can agency nurses claim and what refunds can you hope to receive?

Typically, travel expenses incurred during working hours are tax deductible. These include any journeys made on the same day to perform any required duties (e.g. travelling between assignments), as each destination is deemed to be a temporary workplace. This rule can benefit healthcare professionals in more mobile roles, such as community nurses and homecare workers.

Agency nurses may also be able to claim travel expenses when travelling between the premises of two or more end clients over the course of a single day, providing both end clients were obtained through the same agency; the agency worker must also begin and end the day at their own home.

Some employers may pay towards your travel expenses, however, this is not common amongst umbrella companies. If your employer does not reimburse you for the full amount, any difference may attract some tax relief.

Should you use your own vehicle to make journeys between appointments, there is a statutory of tax-free approved mileage allowances available. This is to compensate for essentials like fuel and general vehicle wear and tear. If you are paid less than these amounts by your employer, you can claim tax relief on the unused balance, reducing the amount that you pay in tax and National Insurance.

Expenses can also be claimed if you travel between appointments by train, bus or any other method of transportation. An allowance will generally be money that has not been reimbursed by your employer.

To be eligible for any relevant tax relief, you will need to retain proof that you travelled between destinations during your time working for the agency. This information should be available through your agency, umbrella company or Accountant.

Please note, tax relief can only be claimed if your total earnings in a single tax year exceed your Personal Allowance, the lowest level at which you must pay tax.

While travel expenses can be claimed for journeys made between assignments, mileage generally cannot be claimed for travel between your home and your place of work (and vice versa). This is due to legislation introduced in April 2016 which restricts certain workers from claiming home to work travel expenses. These include those personally providing services to another person, those employed through an agency or umbrella, or those under the supervision of any person.

Your status under IR35 is a good guide on whether or not you can claim for mileage. If your role is classified as working inside IR35, claiming for daily travel to work may be difficult. The view HMRC takes is that regular/daily travel to work should not be a deductible expense as regular PAYE employees cannot claim this for tax relief either.

However, some travel may be deductible, therefore we recommend you seek confirmation from your accountant around your specific circumstances.

It isn’t just work-related travel that nurses can claim on expenses. Additional costs that can be claimed through tax relief include RCN membership fees (up to 20 per cent), NMC registration fees and uniform costs (including laundering costs).